Climate Smart Ag Newsletter #14

Climate Smart Ag Newsletter #14

Based on a weekly screening of articles, this is the newsletter to keep you updated about the mains news around climate smart agricultural solutions.

This week, articles put in context what is a green premium and why it is justified, what carbon credits buyers are looking for and consequently how we can forsee a more segmented carbon credits market, and consequently what are the related risks for the carbon credits coming from agriculture.

Articles of this week :

Microsoft’s million-tonne CO2-removal purchase — lessons for net zero I Nature

Carbon credit sales are booming: It’s time to calibrate, not celebrate I Substack

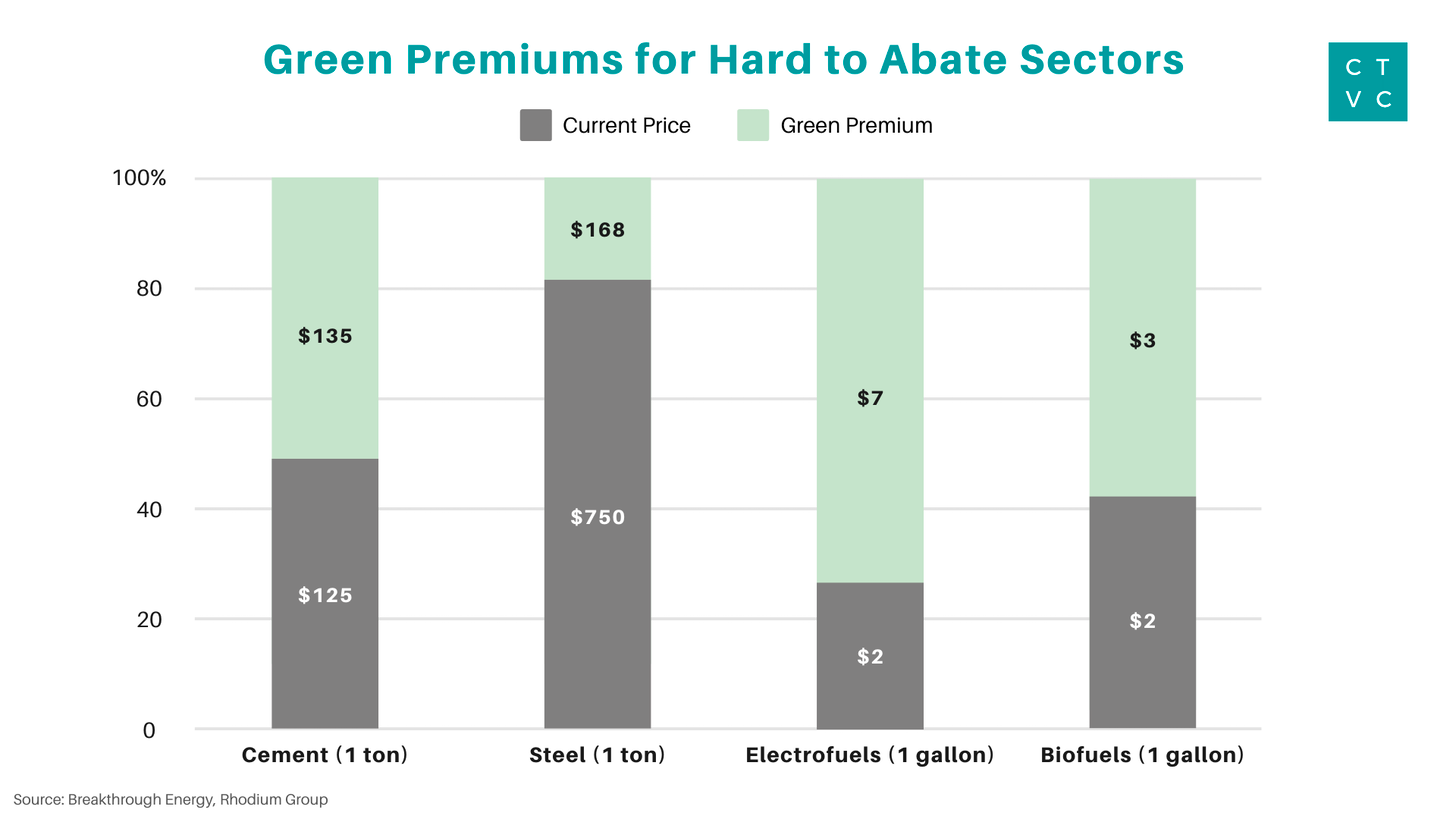

Introducing the Green Premiums | Bill Gates

What is the difference in cost between a product that involves emitting carbon and an alternative that doesn’t? This difference in cost is what I call the Green Premium, and understanding it is key to making progress on climate change.

Since airlines would not be willing to pay more than twice as much to fuel their planes—and many customers would balk at the resulting increase in air fares—the Green Premium on biofuels suggests that we need to find ways to either make them cheaper or make jet fuel more expensive. Or a combination of the two.

Green Premiums exist because fossil fuels don’t factor their impact for warmering the planet. That the reason why clean alternatives appear more expensive.

They help us measure our progress toward eliminating carbon emissions. The bigger a Green Premium is, the further we are from a zero-carbon future.

They serve as a guide to action. In cases where the Green Premiums are big, we know we need innovations that will close the price gap. In cases where they’re small—or where clean products are actually cheaper than the polluting version—it suggests that something other than the cost is keeping zero-carbon products from being deployed, and we need to understand why.

Once we know what’s driving a given Green Premium, it acts like a roadmap—it tells us the route we need to take to get to zero.

We are going to see Green Premium in agriculture for low carbon/regenerative grain production the same way with FMCG that committed for net zero. Some like Nestle have committed for envelope for premium distribution for many raw materials produced using regenerative agriculture practices and also help for investment.

In a previous posts, I shared the example of Saipol that introduced a green premium in the French biofuel market based on low carbon oilseed rape sourcing.

Green premium will enable also to develop the hydrogen economy in the energy sector.

🌍 Industrial first movers will buy low-carbon #74

This article came initially following the creation by John Kerry of a First Movers Coalition

For the Coalition, Kerry is recruiting industry titans from the hardest to decarbonize sectors. Kerry is strategically targeting the last slice of the emissions pie that’s the hardest to abate. A paper published in Science estimates that 15% of global CO2 emissions come from these segments: iron and steel (5%), cement (4%), shipping (3%), aviation (2%), and long-distance road transportation (1%).

They explained next how this is leading to the chicken and egg problem of the supply of demand, where currently the supply is not enough in term of amount and quality.

They also added that the cost of the premium, it can be quite small at the consumer level.

Microsoft’s million-tonne CO2-removal purchase — lessons for net zero I Nature

The aim is that, by 2030, the company will be carbon negative. By 2050, it will have removed all of its emissions since it was founded in 1975. By 2030, the company will reduce its emissions by half or more, and will have 100% of its electricity consumption matched by zero-carbon energy purchases. It will electrify its vehicle fleet, stop using diesel for backup energy and reduce emissions across its value chain. Emissions that are harder to abate, including historical emissions, will be compensated for by withdrawing carbon from the atmosphere.

Here we summarise the lessons learnt shared in the post :

The supply of solutions capable of removing and storing carbon viably is a tiny proportion of that needed to reach global net-zero emissions by 2050,

The scarcity of proposals that met the companies’ criteria reflects a lack of standards and clear definitions

Roughly one-fifth of proposals to Microsoft focused on avoiding new emissions, not on withdrawing CO2 from the atmosphere; these were rejected. Others lacked the technical information needed to ensure reliability

systems for accounting for carbon removal do not distinguish between short- and long-term forms of CO2 storage

Nature-based storage projects sequestering carbon for less than 100 years accounted for most proposals that Microsoft but is cheaper and easier to establish trees and enrich soils than to deploy nascent technologies that capture carbon and store it geologically.

Let’s Not Become the Junk Bonds of Carbon Offsets I Deveron

We incorrectly assumes that all carbon offsets are created equal.

Other industries’ offsets hold two key advantages over agricultural offsets: permanence and accuracy. Without addressing these issues, soil-based carbon offsets will settle at the lower end of the value spectrum.

With a fundamental permanence handicap, the industry is at a critical decision-making point when it comes to the accuracy (how closely the carbon offset sold reflects the actual carbon stored) of its offsets.

The author in this article highlights how it is important to remember that ag carbon credit are part of a broader market as shown in the previous artivles, with different technologies. We have to ensure that we can tackle this in order to ensure that ag carbon credits don’t become the “Junk Bonds “.

Carbon credit sales are booming: It’s time to calibrate, not celebrate I Carbonware

The autor introduced a carbon market mental model based on among others things on the conclusion from Microsoft from their removal purchase. This is a great article that explain the risk shred in the previous article.

We essentially have different markets with different buyers, different sellers, and very different rules. Here’s my mental model for thinking about this market:

#1 the bleeding edge is the quality contingency. This is where Stripe, Microsoft, Climeworks, Breakthrough Energy Ventures, and other climate tech VCs and startups are playing. It’s a hotbed of innovation. They’re partnering with world-renowned experts to write new rules for what high-quality climate action looks like.

On the other hand is #3 the voluntary commodity market. It’s the largest voluntary segment, and as a result of its size, it’s basically what we see in the Ecosystem Marketplace report.

In the commodity segment, almost any offset that meets the rules set by a carbon registry (e.g., American Carbon Registry, Gold Standard, Verra) is eligible for purchase and trade. In spite of the best intentions of these standard-setting organizations, with that as the bar, this segment tends to be a race to the cheapest: “The simplest and least costly project that generates readily the largest volumes of credits crowd out more worthy, complex, costly ventures.”

It will be interesting to see how the ag carbon market will evolve in a market that will consequently increasingly be segmented, with more quality credits.